Getting personal property insurance is something that people only sometimes consider. Today, we look into why you should consider this coverage, aside from insuring your home and the advantages of property insurance.

What Is Property Insurance and Why You Should also Look at its Advantages?

Property insurance is a type of insurance that provides property protection and liability coverage for property owners. It is important to understand why property insurance is necessary and why it is essential to protect against unexpected events. It can include several policies such as homeowners insurance, renters insurance, flood insurance, and earthquake insurance. Personal property insurance is usually part of homeowners’ or renters’ policy and is very high value and costly. An insurance company must guarantee that the company will bear the burden of a significant loss if there is a loss in the future. Property insurance can also protect against damaging or losing costly personal property.

Homeowners Insurance 101

Key Points and the Advantages of Property Insurance

- Property insurance is a group of policies that offers property protection or liability coverage.

- It can include several policies such as homeowners insurance, renters insurance, flood insurance, and earthquake insurance.

- It is recommended for those who own expensive property and is often combined with liability insurance.

- However, it does not cover your property equally, such as jewelry, which may need additional floater coverage.

How much coverage do I have?

There are two kinds of personal property coverage. These are the replacement cost and actual cash value. A replacement cost insurance policy usually pays the dollar amount needed to purchase a new item when you place a claim. Meanwhile, an Actual Cash Value insurance policy works in depreciation to offer you a reimbursement based on the current value of an item. It’s also essential to point out that personal property coverage limits what it will pay to replace an item or a group of items.

Does Renter Insurance cover my insurance?

People need to understand renter insurance. They believe their landlord’s insurance policy will also cover their personal belongings. Landlord insurance usually will help protect your residence against certain risks. However, this coverage usually does not cover a renter’s belongings. The personal property coverage included in a renters policy will help protect your belongings, such as your cameras and laptops. This is up to the coverage limits in your policy.

We make it easy to compare homeowners insurance quotes so you can find the perfect fit for your home.

Does Condo Insurance Cover My Belongings?

A standard condo policy will also include insurance coverage for the owner’s personal belongings against risks such as fire or theft. However, this protection does not extend to the things inside a unit, even though a condo association’s insurance may also help protect the physical structure of the building and the areas shared by multiple owners. A condo owner’s insurance policy will help safeguard your personal belongings, such as furniture, computers, or clothing, against a covered loss. We again repeat that coverage limits will also apply. We can help you understand more about this, so please don’t hesitate to contact us.

Does Homeowners Insurance Cover My Personal Property?

Most homeowners insurance policies will include coverage for personal property. This is in addition to also providing dwelling and liability protection up to the limits of the insurance policy. So, let’s say your home obtains damages such as covered perils like a fire. For example, homeowners insurance will pay to repair the damage to the home structure and help replace your personal belongings. Kindly note that the insurance coverage is subject to the terms and limits stated in your policy, so please always read your policy or feel free to ask us if you have any clarifications or other inquiries.

Does Insurance Cover Lost Items?

Usually, homeowners, renters, and condo insurance policies do not cover your lost personal belongings. If one of your personal properties gets stolen, you’ll have to find insurance to help cover the loss. However, suppose you misplace a specific item or you happen to leave one of your belongings in a hotel room, for example. In that case, your insurance policy will not cover the loss. However, you can purchase add-on protection such as a scheduled personal property for particular items. This may then help you cover the lost items. We suggest talking to us to learn more about this.

Does Insurance Cover Jewelry?

Jewelry is usually personal property. However, it’s essential to consider whether your coverage limits are high enough to protect your valuable jewelry the most. Most often, insurance policies will have sub-limits for certain kinds of belongings, such as your jewelry. Coverage for jewelry may be more limited, while your overall personal property coverage limits are higher. Always check your insurance policy or ask us questions about what kind of coverage you have in place for your jewelry.

What Is a Scheduled Personal Property?

Always remember that the coverage for homeowners, renters, or condo policy usually comes with sub-limits for specific kinds of property. Sometimes, there are even limits for each item, even though this may offer you protection for your personal belongings. We can help you decide whether you may take advantage of scheduling certain items. This means buying separate coverage to protect specific high-value items, such as jewelry, art, or musical instruments.

What Isn’t Part of Personal Property Coverage?

Personal property coverage applies when your personal belongings obtain damaged by certain risks. It’s essential to note that not all kinds of risks are part of a basic insurance policy. For example, if your personal belongings get damaged by flood, your personal property coverage in homeowners, condo, or renters insurance policy would not offer you reimbursement. However, suppose you have a separate flood insurance policy. In that case, you can file a claim for items damaged by a flood in your home. We greatly suggest you ask us any questions regarding what risks your insurance may or may not cover.

It’s essential to know what kind of coverage you have if something unexpected happens since your personal belongings’ value can add up. We can help you review your insurance policy and let you know what other kinds of coverage may be available to help you better protect what’s important to you.

What Kinds of Damage Does Personal Property Insurance Cover?

Coverage limits may differ with each insurance policy. There are two kinds of homeowners/renters/condo insurance policies: open peril and named peril. They decide which kinds of damage are part of your coverage.

Policies With Named Perils

Standard homeowners insurance policies cover belongings against named perils, but must be destroyed to file a claim.

- Lightning or fire

- Hail or windstorm

- Damage caused by aircraft

- Explosions

- Riots or civil disturbances

- Smoke damage

- Damage caused by vehicles

- Theft

- Vandalism

- Falling objects

- Volcanic eruption

- Damages caused by the weight of snow, ice, or sleet

- Water damage from plumbing, heating, or air conditioning overflow

- Water heater cracking, tearing, and burning

- Damage from electrical current

- Pipe freezing

The most important details are that you will be covered if your couch is destroyed from a pipe in your ceiling or your fridge gets burned. Still, you are not if a wild animal runs over your living room. You must opt for an “open peril” policy to avoid this.

Home fire safety is important. But did you know you can save money by installing active home fire safety features?

Open peril policy

Open peril insurance policies safeguard your personal belongings from any kind of damage as long as they’re not part of your insurance policy. Basic homeowners/condo policies usually exclude the coverage for the following:

- Natural settling, cracking, shrinking, or expansion of the foundation

- Earthquakes and floods

- Pressure from tree roots

- Faulty construction

- Insects, vermin, rodents, and pet damage

- Natural wear and tear

- Mold

- Corrosion

For instance, if your clothing or furniture obtains damages in an earthquake, you would not be eventually covered. However, in our previous example of a wild animal entering your home, you’re not explicitly excluded from that. You would be part of the coverage since your insurance company can’t prove that your policy excludes the cause of the damage.

Actual cash value vs. replacement cost value for Property Insurance and its Advantages

Basic homeowners policies pay for the actual cash expense of belongings if they’re destroyed in a covered incident, but only up to their current value minus the depreciation. A replacement-cost value or RCV policy pays for the current market price for an item, even if it has already depreciated. For example, if you file a claim with the RCV policy, you would get the full $1,000 to replace your TV.

Get free Home and Auto Insurance Quotes from the top leading companies. Start Here!

Does Homeowners Insurance Cover Damaged or Lost Jewelry?

Insurance policies can only cover up to a certain amount of jewelry. Still, other high-value items such as musical instruments, electronics, laptops and phones, and cash can be insured up to $5,000. To increase the value of these items, you must buy an endorsement from your insurance company. You can also apply for other insurance policies for these items.

How Property Insurance Works and its Advantages

Property insurance covers property structure and its contents, as well as liability coverage if the property owner or renter is injured. It also covers weather-related incidents, tsunamis, floods, drain and sewer backups, seeping groundwater, standing water, and other sources of water.

Personal property can be filed online or over the phone, and if approved, the insurance company will provide reimbursement in two stages. The insurance company may also reimburse the extra expense if the item is damaged more than expected. It is essential to save receipts and statements before any purchases are made.

Understanding Property Insurance and its Advantages

Property insurance coverage is divided into three types: actual cash value, replacement cost, and extended replacement costs. Actual cash value covers the owner or renter for the replacement expenses minus the depreciation. In contrast, replacement cost covers repairing or replacing property at equal value. Extended replacement costs pay more than the coverage limit if the expenses for the construction have increased. The limit is the maximum amount of the benefit the insurance company will pay you for a given situation.

Special Considerations about Property Insurance and its Advantages

Most homeowners opt for a combination of insurance policies to compensate for physical loss or damage caused by numerous perils, such as fire, vandalism, and theft. The coverage called HO3 policy has a limit on the coverage of certain valuables and collectibles, and no insurance coverage is usually given for accidental breakage/damage and mysterious disappearances. HO5 homeowners coverage includes everything included in an HO3 policy, but is leaning towards the structure and the home’s property, including furniture, appliances, clothing, and other personal items. HO4 property insurance is also renter’s insurance, but does not cover the rented house or apartment. Home warranties are another way to safeguard your property and can be helpful for you.

For a safe, reliable and fair home and car insurance coverage for you, get free quotes from top companies now!

The Importance of Property Insurance and its Advantages

Who Needs Property Insurance?

People who own expensive property should purchase property insurance to avoid financial issues if their car is damaged in an accident. All states require drivers to carry auto insurance in the form of liability insurance, which covers the repair and financial replacement of someone else aside from the individual involved. When you opt for required liability coverage, you can also opt for comprehensive and collision insurance regarding auto insurance.

Coverage of Property Insurance and its Advantages

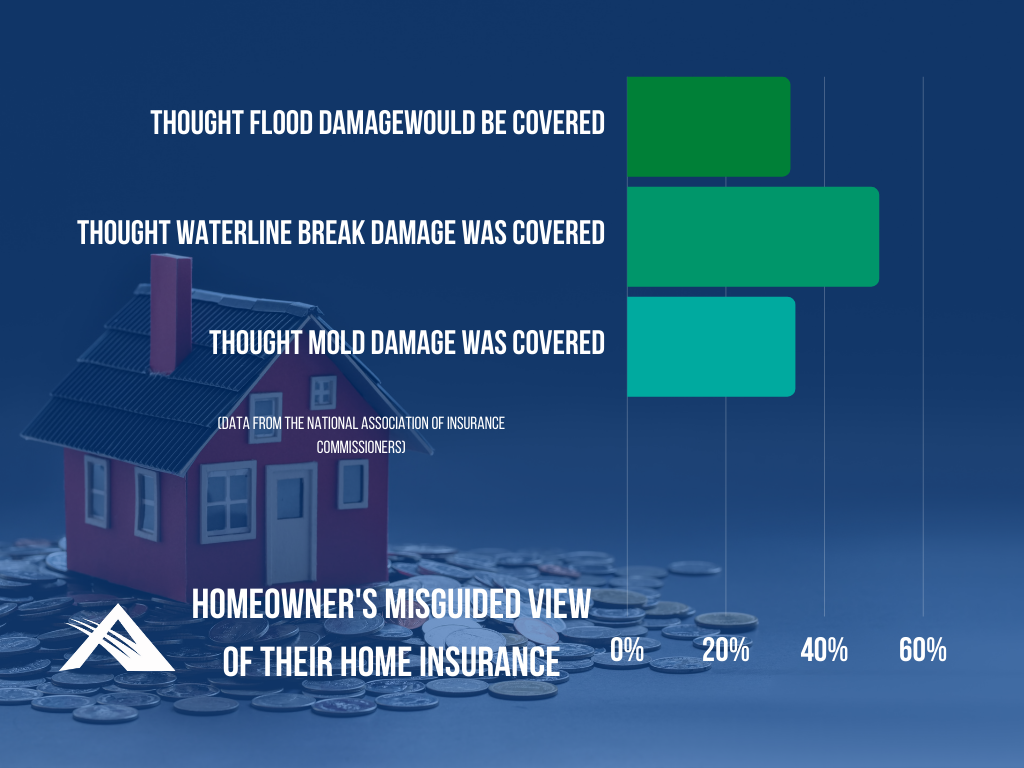

Many homeowners have a variety of misguided views of what their homeowner’s insurance actually covers according to a survey published in the Journal of Financial Planning. Roughly 33% of homeowners in the survey thought that flood damage would be covered by their policy, while around 51% of the respondents thought that their home’s main water line break damage would be covered, and finally, 34% of them thought mold damage was covered by their insurer. These data are from the National Association of Insurance Commissioners.

In reality, the perils, which are causes of property destruction, that are usually not covered are:

- Flood damage (this is a separate policy)

- Earthquake (this is also a separate policy)

- Mold Maintenance damage (examples are worn-out plumbing, electrical wiring, air conditioners, heating units, roofing, mold, and pest infestation)

- Sewer backup

Policies are usually written so that it must be sudden and accidental for something to be covered. This means that it wasn’t just a slow leak that caused the damage for many months. This is usually not covered by insurance. It will not be covered if your roof gets destroyed due to old age, not from storm damage.

The perils that are normally covered are:

- Fire or lightning

- Windstorm or hail

- Explosion

- Smoke

- Theft

- Vandalism or malicious mischief

- Riot or civil commotion

- Damage caused by aircraft or vehicles

- Volcanic eruption

Liability Coverage

Many insurance policies include liability coverage in addition to covering the value of the home or other property. Liability coverage is well known to people who own automobiles but is lesser known to homeowners. It includes paying for the damage caused by the fire if your neighbor’s house catches fire, paying for medical attention if someone gets hurt, and reimbursing for stolen property. It is essential to document how the theft happened and give a police report to your insurance company, as well as know what your policy does and does not cover. Insurance companies only stay in business by asking for a minimal amount to cover anything that can happen to your property.

Homes are the place where we find our peace after a hard day at work, and auto insurance can be that protection from countless auto accidents and mishaps. When you combine home and auto insurance policies into a bundle, you save on both.

Additional (Non) Coverage

Home-based businesses are usually not covered. This doesn’t come with the home study but a place where people get together into your home as customers like a workshop where you repair furniture. You will need a separate business commercial policy to ensure this particular area and its connected liability. These rules differ from every state and every country. Also, if your property, especially your home is vacant for a long time usually at around 30 days, then the homeowners’ policy may be canceled as soon as possible by your insurance company. It will be assumed that a vacant home is much more risked with more perils such as fire and theft hence changing the risk profile enough to require another separate insurance policy. You may get another insurance policy to cover this home as well if you have a second home or vacation property.

Important to take note: Kindly be aware of how your policy covers repairs. Always covering the full replacement expenses is much better than just the actual cash value (ACV). However, this will cost you more in premiums.

Pitfalls to Avoid

We suggest that you always check if your policy covers repairs at actual cash value or at replacement expenses. The latter is usually much better. One sample is if your roof was damaged and needs to be completely changed, the replacement expenses will pay for the replacement and this is less your deductible. This is while your actual cash value will pay you what your roof was estimated to be actually worth at the time of the damage. The tradeoff is that your actual cash value is less than replacement cost coverage.

Art and Jewelry

In addition, if you have expensive jewelry or art that you want to be covered, you may have to obtain a floater. This is an add-on to your main insurance policy. Many insurance policies have basic amounts that they will pay out for losses to specific items and they will pay no more.

Coinsurance Clauses

It is important to also note that some property owners only want to insure a property for what they actually paid for which may lead to a coinsurance clause. This will depend on local laws of your state where the property is currently insured for less than about, for example, 80% of its current replacement expenses. You will have a lesser amount of coverage and your insurance company will require you to share in a percentage of the repairs above and more than the deductible amount.

Get a free quote with a bundling discount on home and auto insurance. Make shopping for auto insurance easier and save money!

Premium Factors

Here are a few questions to consider:

- Does your area always experience tornadoes, hurricanes, or floods?

- Do you also own a large dog or a swimming pool?

- Do you also smoke?

- How’s also your credit score?

If your answer to these questions is “yes,” you must be a higher-than-normal risk, and an insurance company will charge you accordingly. These are some factors it will consider when setting your insurance premium rates. The higher your rates, the more these and other risks will apply to you.

A Word of Warning about Property Insurance

The most critical details in this text are that when looking for property insurance, it is vital to check the company’s reputation and carefully study its insurance policy. It is also important to remember that cheap insurance can be costly and that high-quality coverage is often the legal minimum in a location. Property insurance has a lot of advantages but also a lot of disadvantages.

Ask us anytime!

We hope you learned a lot about the advantages of property insurance. Give us a try, and you won’t be sorry. If you have any questions, please do not hesitate to contact us at Team AIS in Denver, CO. We will be waiting!